What You Need To Find Out About Mortgages For Your Home

Article written by-Skov HoffmanWhile everyone considers buying a home at some point in their life, having to get a mortgage to pay for it can seem intimidating. In fact, some people are so worried about the situation that they continue to rent instead. Build your confidence by reading this article and learning about mortgages.

Predatory lenders are still in the marketplace. These lenders usually prey on home buyers with less than perfect credit. They offer low or no down payments; however, the interest rates are extremely high. Additionally, these lenders often refuse to work with the homeowner should problems arise in the future.

Gather all needed documents for your mortgage application before you begin the process. These documents are the ones most lenders require when you apply for a mortgage. Income tax returns, W2s, bank statements and pay stubs are usually required. If you have the documents in hand, you won't have to return later with them.

Think about getting a consultant hired if you wish to get help with your home mortgage. There is much to learn in this process, and they can help you obtain the best deal you can. They can also make sure your have fair terms instead of ones just chosen by the company.

Get mortgage loan estimates from at least three different mortgage lenders and three different banks. By shopping around, you may get a lower interest rate, pay fewer points and save money on closing costs. It's almost always preferable to get a fixed interest rate. With variable rates, you may not know from month to month what your mortgage payment will be.

When you decide to apply for a mortgage, make sure you shop around. Before deciding on the best option for you, get estimates from three different mortgage brokers and banks. Although, interest rates are important, there are other things you should consider also such as closing costs, points and types of loans.

Predefine terms before your application process, not just to prove to your lender that you are able to handle any arrangements, but also to keep it within your monthly budget, too. This means setting a limit for monthly payments, based on what you can afford and not just what type of house you want. Regardless of a home's beauty, feeling house poor is no way to go through life.

If you are a veteran of the U.S. Armed Forces, you may qualify for a VA morgtage loan. These loans are available to qualified veterens. The advantage of these loans is an easier approval process and a lower than average interest rate. The application process for these loans is not often complicated.

Remember that your mortgage typically can't cover your entire house payment. You need to put your own money up for the down payment in most situations. Check out your local laws regarding buying a home before you get a mortgage so you don't run afoul of regulations, leaving you homeless.

Make sure you pay down any debts and avoid new ones while in the process of getting approved for a mortgage loan. Before a lender approves you for a mortgage, they evaluate your debt to income ratio. If your debt ratio is too high, the lender can offer you a lower mortgage or deny you a loan.

Before you apply for a mortgage, know what you can realistically afford in terms of monthly payments. Don't assume any future rises in income; instead focus on what you can afford now. Also factor in homeowner's insurance and any neighborhood association fees that might be applicable to your budget.

If you can afford the higher payments, go for a 15-year mortgage instead of a 30-year mortgage. In the first few years of a 30-year loan, your payment is mainly applied to the interest payments. Very little goes toward your equity. In a 15-year loan, you build up your equity much faster.

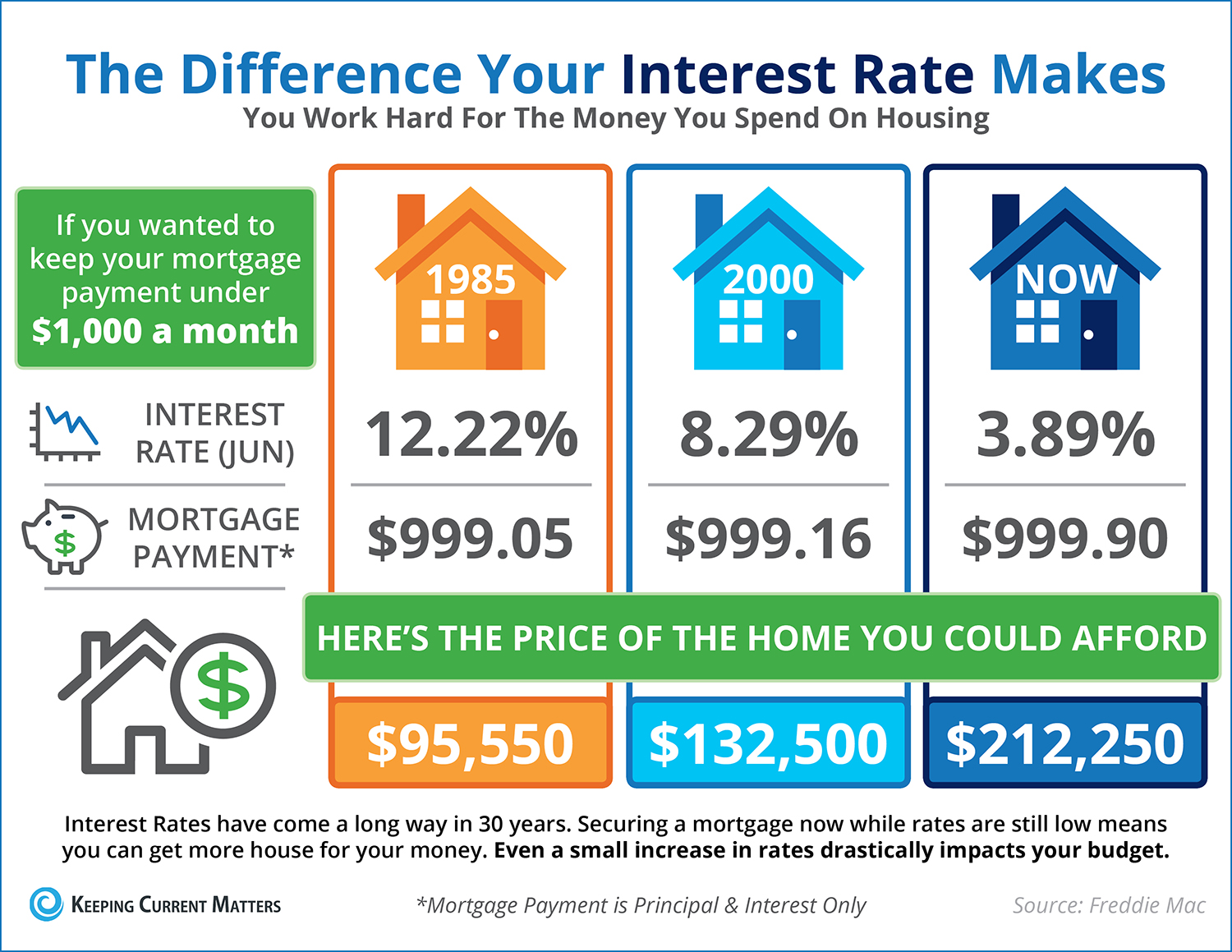

Mortgage rates change frequently, so familiarize yourself with the current rates. You will also want to know what the mortgage rates have been in the recent past. If mortgage rates are rising, you may want to get a loan now rather than later. If the rates are falling, you may decide to wait another month or so before getting your loan.

Keep closing costs in mind. You might be focused totally on the excitement of beginning your homeownership. But, you are more than likely going to have to cover a few percentage points of the closing costs of the mortgage in order to secure the deal. Know how this works in your locality and be ready to spend.

Before you apply for a mortgage, know what you can realistically afford in terms of monthly payments. Don't assume any future rises in income; instead focus on what you can afford now. Also factor in homeowner's insurance and any neighborhood association fees that might be applicable to your budget.

Sellers know you are truly motivated to buy when you are prepared with a letter indicating you are approved for a home loan. This tells the seller that you have the financial wherewithal to get the loan and that you are serious. https://business.chase.com/resources/manage/managing-small-business-hr look at homes that go over the preapproval number. If it goes higher, then the seller is going to expect more.

You can save money on a mortgage by going with a lender who offers to finance with no closing costs. Closing costs are a significant part of a mortgage. To make up for that lost money, however, the lenders will make up it in some other way. Usually with a slightly higher interest rate.

If you come into some money for any reason, do not go on a spending spree. The best investment you can make is in your home. Use unexpected cash to pay down your mortgage quicker. This means you have to pay less interest. It also lets you become the true homeowner sooner.

Understanding the principles of a solid mortgage helps you get the best mortgage for your particular financial situation. Getting a home loan is a major commitment, and you never want to get yourself into an uncomfortable bind. Instead, you want a comfortable mortgage with a company that is going to take care of its homeowners.